The digital payments landscape has evolved rapidly over the past decade, with businesses increasingly adopting contactless payment technologies to provide faster, more convenient, and secure customer experiences. One of the most significant innovations in this space is SoftPOS (Software Point of Sale), which enables merchants to accept contactless card payments directly on NFC-enabled Android smartphones or tablets without requiring dedicated POS hardware.

SoftPOS offers numerous advantages, including lower deployment costs, simplified merchant onboarding, greater mobility, and faster scalability for banks, payment service providers (PSPs), fintech companies, and retailers. However, unlike traditional payment terminals that use tamper-resistant hardware, SoftPOS operates on commercial off-the-shelf (COTS) Android devices. This introduces unique cybersecurity challenges that must be addressed to protect payment data, merchant credentials, and customer information.

To build trust in software-based payment acceptance, organizations must implement a multi-layered security strategy. Technologies such as Device Attestation, End-to-End Encryption (E2EE), Multi-Factor Authentication (MFA), Tokenization, Secure Key Management, Runtime Application Protection, and Continuous Monitoring work together to safeguard transactions and maintain compliance with industry standards like PCI MPoC and EMV.

In this guide, you’ll learn the essential SoftPOS security best practices, how they protect digital payment ecosystems, and why they are critical for secure, compliant, and scalable payment acceptance.

What Is SoftPOS Security?

SoftPOS security refers to the collection of technologies, processes, and controls that protect payment transactions processed through software-based point-of-sale applications running on Android devices. Since these devices are general-purpose smartphones or tablets rather than dedicated payment terminals, they require multiple security mechanisms to ensure that cardholder data remains confidential and that transactions cannot be altered or intercepted.

A secure SoftPOS solution protects the entire payment lifecycle—from the moment a customer taps a contactless card or mobile wallet on the device until the transaction is securely authorized by the acquiring bank.

Unlike traditional POS systems that primarily rely on specialized hardware security modules, SoftPOS combines hardware capabilities, operating system protections, cryptographic techniques, and cloud-based security services to create a trusted payment environment.

Why Does SoftPOS Need Strong Security?

Payment applications process highly sensitive information, including payment credentials and transaction data. If a SoftPOS device is compromised, attackers may attempt to access or manipulate this information, leading to financial losses, fraud, and regulatory penalties.

Strong security is therefore essential to:

- Protect cardholder and merchant data from unauthorized access.

- Prevent fraud caused by malware, rooted devices, or stolen credentials.

- Ensure payment transactions cannot be modified during processing.

- Verify that only trusted devices and authenticated users can process payments.

- Meet compliance requirements defined by PCI Security Standards Council and EMV specifications.

- Build customer confidence in contactless payment acceptance.

Implementing multiple layers of protection significantly reduces the likelihood of successful cyberattacks while ensuring uninterrupted payment services.

Why Is SoftPOS Security Important?

Growing Cybersecurity Threats in Digital Payments

As digital payments continue to expand worldwide, cybercriminals are increasingly targeting mobile payment applications. Attack methods have become more sophisticated, making proactive security measures essential for every organization deploying SoftPOS solutions.

Common security threats include:

Malware Attacks

Malicious software can attempt to steal payment information, capture screen data, intercept communications, or manipulate transactions.

Rooted or Jailbroken Devices

Devices with elevated privileges bypass Android’s built-in security controls, increasing the risk of unauthorized access to sensitive payment information.

Application Tampering

Attackers may modify the SoftPOS application to bypass security controls, disable encryption, or inject malicious code.

Man-in-the-Middle (MITM) Attacks

Hackers may intercept communication between the SoftPOS device and backend systems if secure encryption and certificate validation are not implemented.

Credential Theft

Weak authentication methods can expose merchant accounts, administrative portals, or backend systems to unauthorized access.

API Exploitation

Poorly secured APIs can become entry points for attackers attempting to manipulate transactions or retrieve sensitive information.

Business Risks of Weak SoftPOS Security

Inadequate security can have serious operational, financial, and reputational consequences.

Organizations may face:

- Financial fraud resulting from unauthorized transactions.

- Data breaches exposing sensitive customer information.

- Non-compliance with PCI or EMV security requirements.

- Regulatory fines and legal liabilities.

- Increased operational costs due to fraud investigations.

- Loss of customer trust and merchant confidence.

- Damage to brand reputation and business credibility.

Investing in strong security controls helps organizations mitigate these risks while ensuring long-term business sustainability.

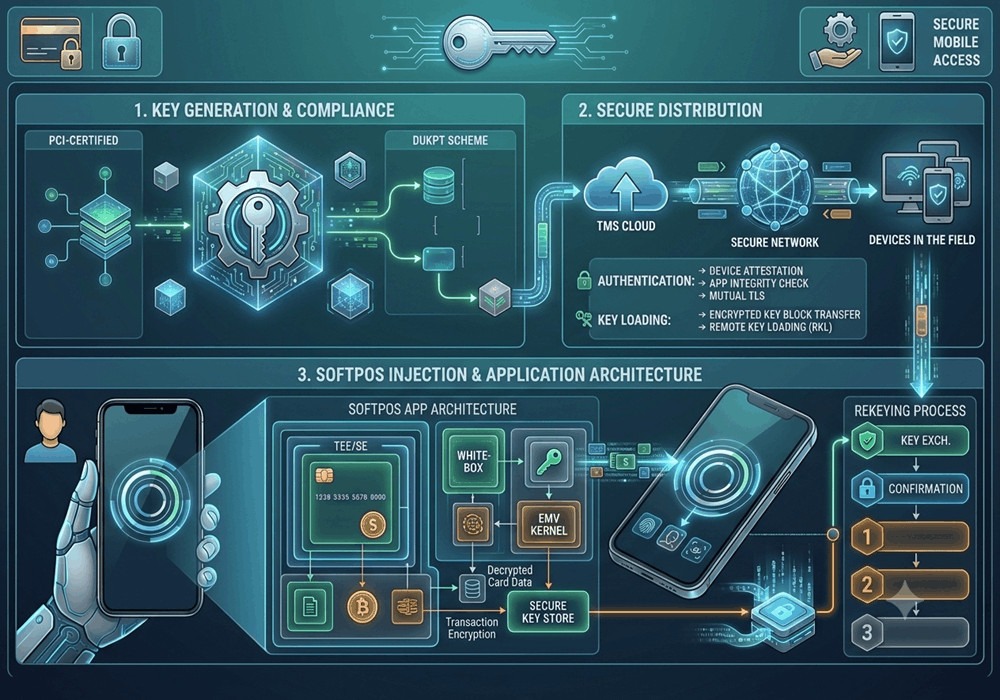

Core Components of a Secure SoftPOS Architecture

A secure SoftPOS ecosystem is built on multiple interconnected security layers. No single technology can protect every aspect of the payment process, so organizations should adopt a defense-in-depth approach.

Key components include:

Secure Android Device : The payment device should run a trusted operating system, receive regular security updates, and support hardware-backed security features where available.

SoftPOS Payment Application: The application should be digitally signed, protected against tampering, and designed with secure coding practices to minimize vulnerabilities.

Device Attestation: Before processing transactions, the application verifies that the device has not been rooted, modified, or compromised.

Encryption Layer: Sensitive payment data should be encrypted both during transmission and while stored on the device.

Multi-Factor Authentication (MFA): Merchants and administrators should use multiple authentication factors to access payment applications and management portals.

Secure APIs: Communication between the SoftPOS application, Terminal Management System (TMS), payment gateway, and backend services should be protected using authenticated APIs and modern TLS encryption.

Terminal Management System (TMS)

A centralized TMS enables secure device provisioning, configuration management, certificate distribution, remote updates, and compliance monitoring.

Payment Gateway and Acquiring Bank: Transactions are securely routed through the payment gateway to the acquiring bank for authorization, ensuring payment integrity and interoperability. Together, these components create a resilient security architecture capable of protecting payment transactions from a wide range of cyber threats.

Device Attestation: The First Line of Defense

What Is Device Attestation?

Device attestation is one of the most critical security controls in a SoftPOS environment. It is the process of verifying that the Android device attempting to process payments is genuine, uncompromised, and operating in a trusted state.

Rather than assuming every smartphone is secure, the SoftPOS application performs a series of integrity checks before allowing payment transactions. These checks help identify rooted devices, modified operating systems, malware infections, or other conditions that could expose sensitive payment data.

If a device fails the attestation process, payment functionality can be restricted or blocked until the security issue is resolved.

How Does Device Attestation Work?

Device attestation typically follows a structured verification process:

- Device Registration: The device is enrolled and associated with an authorized merchant account.

- Integrity Verification: The operating system and application integrity are validated to ensure they have not been modified.

- Root Detection: The system checks whether the device has been rooted or jailbroken.

- Bootloader Verification: The bootloader status is examined to detect unauthorized modifications.

- Application Validation: Digital signatures and application hashes are verified to confirm authenticity.

- Trust Assessment: The results of all security checks are combined to determine whether the device is trusted.

- Payment Authorization: Only devices that successfully pass the attestation process are permitted to process payment transactions.

Key Security Checks Performed During Device Attestation

Root Detection: Rooted devices bypass Android’s standard security protections, making it easier for attackers to access sensitive payment information. Detecting and blocking rooted devices significantly reduces the attack surface.

Bootloader Verification: An unlocked bootloader may allow unauthorized software to be installed on the device. Verifying the bootloader status helps ensure that the operating system has not been tampered with.

Operating System Integrity: The SoftPOS application verifies that the device is running a genuine and up-to-date operating system, reducing the risk of vulnerabilities introduced by unofficial firmware.

Malware Detection: Security checks identify suspicious processes, unauthorized applications, or known malware signatures that could compromise payment data.

Application Integrity Verification: The application validates its own digital signature and integrity to ensure that attackers have not modified the software or injected malicious code.

SoftPOS Security Best Practices: Device Attestation, Encryption & MFA

Encryption in SoftPOS

What Is Encryption?

Encryption is one of the most fundamental security technologies used in SoftPOS solutions. It converts sensitive payment information into an unreadable format using advanced cryptographic algorithms, ensuring that only authorized systems with the correct decryption keys can access the original data.

Every contactless payment transaction involves the exchange of confidential information, such as card credentials, transaction details, and authentication data. Without encryption, this information could be intercepted by cybercriminals while it is stored on the device or transmitted across communication networks.

Encryption protects payment information throughout the transaction lifecycle, making it nearly impossible for attackers to read or misuse intercepted data. It is a critical requirement for PCI standards and forms the backbone of secure digital payment infrastructure.

Why Is Encryption Important in SoftPOS?

Since SoftPOS operates on commercial Android smartphones rather than dedicated payment terminals, encryption plays a vital role in protecting sensitive payment data against modern cyber threats.

A robust encryption strategy helps organizations:

- Protect confidential payment information from unauthorized access.

- Prevent data interception during online communication.

- Reduce the risk of financial fraud and identity theft.

- Maintain customer trust in contactless payment systems.

- Meet PCI MPoC, PCI DSS, and EMV security requirements.

- Protect merchant credentials and transaction records.

- Secure communication between devices and backend systems.

- Minimize the impact of potential cybersecurity incidents.

Without strong encryption, even a secure payment application could become vulnerable to network attacks or unauthorized data exposure.

Types of Encryption Used in SoftPOS

Different stages of the payment process require different encryption techniques. Modern SoftPOS solutions typically implement multiple encryption layers to provide end-to-end protection.

End-to-End Encryption (E2EE)

End-to-End Encryption protects payment data from the moment a customer taps their contactless card or mobile wallet until the transaction reaches the payment processor or acquiring bank.

Instead of transmitting plain-text payment information, the SoftPOS application encrypts the data immediately after capture. The encrypted data remains protected throughout its journey across networks and is only decrypted by the authorized payment processing environment.

Benefits of End-to-End Encryption

- Prevents attackers from reading intercepted payment data.

- Protects cardholder information during transmission.

- Reduces the risk of payment data breaches.

- Strengthens compliance with PCI security standards.

- Builds trust among merchants and customers.

Data-at-Rest Encryption

Not all payment-related information is transmitted immediately. Some data may be temporarily stored on the device, such as transaction logs, configuration files, merchant profiles, or certificates. Data-at-Rest Encryption ensures that any information stored locally remains encrypted, making it unreadable even if the device is lost, stolen, or compromised.

Typical data protected includes:

- Merchant profiles

- Device certificates

- Configuration settings

- Transaction history

- Authentication tokens

- Security logs

Data-in-Transit Encryption

Every communication channel within the SoftPOS ecosystem should be encrypted while data is moving between systems.

Communication occurs between:

- SoftPOS application and Terminal Management System (TMS)

- SoftPOS application and payment gateway

- Device and backend servers

- Merchant application and cloud platform

- APIs and banking infrastructure

Modern SoftPOS solutions typically use TLS 1.2 or TLS 1.3 to establish secure communication channels and prevent unauthorized interception.

Common Encryption Algorithms Used in SoftPOS

Several industry-standard cryptographic algorithms work together to secure payment transactions.

AES (Advanced Encryption Standard): AES-256 is widely used for encrypting sensitive payment information because it provides strong security with efficient performance.

Common uses include:

- Payment data encryption

- Local file encryption

- Secure storage

- Configuration protection

RSA (Rivest-Shamir-Adleman): RSA is an asymmetric encryption algorithm commonly used for secure key exchange and digital signatures.

Typical applications include:

- Certificate authentication

- Secure key distribution

- Digital signatures

- Identity verification

ECC (Elliptic Curve Cryptography): ECC offers security comparable to RSA while using much smaller key sizes, making it ideal for mobile payment applications. Benefits include:

- Faster performance

- Lower power consumption

- Reduced bandwidth usage

- Strong cryptographic protection

SHA-256: SHA-256 is a secure hashing algorithm used to verify data integrity rather than encrypt data. It helps:

- Verify software integrity

- Detect file modifications

- Protect passwords

- Generate secure hashes

TLS 1.3: Transport Layer Security (TLS) secures network communication between devices and backend servers. TLS provides:

- Encrypted communication

- Mutual authentication

- Message integrity

- Secure API communication

Encryption Best Practices

Organizations deploying SoftPOS should adopt comprehensive encryption strategies rather than relying on a single encryption mechanism. Recommended practices include:

- Encrypt payment data immediately after capture.

- Never store plain-text cardholder information.

- Use strong, industry-approved encryption algorithms.

- Rotate encryption keys regularly.

- Protect cryptographic keys using secure hardware where available.

- Encrypt all communication channels using TLS.

- Digitally sign applications and firmware updates.

- Regularly audit encryption implementations.

Multi-Factor Authentication (MFA)

What Is Multi-Factor Authentication?

Authentication is the process of verifying a user’s identity before granting access to payment applications or administrative systems.

Traditional username-and-password authentication is no longer sufficient because passwords can be stolen through phishing, malware, or credential leaks.

Multi-Factor Authentication (MFA) strengthens identity verification by requiring users to provide two or more independent authentication factors before access is granted.

Even if one factor is compromised, attackers cannot access the system without the additional verification factors.

Types of Authentication Factors

MFA combines different categories of authentication to improve security.

Something You Know

Knowledge-based authentication includes information known only to the user.

Examples include:

- Passwords

- PIN codes

- Security questions

- Passphrases

Although commonly used, these methods should not be relied upon as the sole authentication mechanism.

Something You Have

Possession-based authentication verifies ownership of a trusted device or physical token. Examples include:

- Registered smartphone

- OTP generated by an authenticator application

- Hardware security token

- Smart card

This additional layer significantly reduces the risk of unauthorized access.

Something You Are

Biometric authentication uses unique physical characteristics to verify identity. Common examples include:

- Fingerprint recognition

- Facial recognition

- Iris scanning

- Voice recognition

Biometric authentication offers convenience while making impersonation much more difficult.

Where Should MFA Be Implemented?

MFA should protect all critical components of a SoftPOS ecosystem. Organizations should require MFA for:

Merchant Login: Prevents unauthorized access to payment applications.

Administrator Access: Protects management consoles and backend systems.

Device Registration: Ensures only approved devices are enrolled.

Configuration Changes: Prevents unauthorized modification of payment settings.

High-Value Transactions: Adds additional verification for sensitive financial operations.

Terminal Management System (TMS): Secures remote device management functions.

Benefits of Multi-Factor Authentication

Implementing MFA provides significant advantages across the payment ecosystem. Key benefits include:

- Prevents account takeover attacks.

- Reduces password-related security risks.

- Protects merchants against phishing attempts.

- Enhances identity verification.

- Supports regulatory compliance.

- Improves customer confidence.

- Reduces fraud-related financial losses.

- Secures remote administration.

Tokenization

What Is Tokenization?

Tokenization is a security technique that replaces sensitive payment information, such as the Primary Account Number (PAN), with a randomly generated token that has no exploitable value outside the payment ecosystem.

Unlike encryption, which can be reversed using a decryption key, tokens cannot reveal the original card data without access to the secure token vault maintained by authorized payment processors. This significantly reduces the exposure of cardholder data and helps organizations minimize the scope of PCI compliance.

Benefits of Tokenization

- Reduces the risk of card data theft.

- Protects customer privacy.

- Minimizes PCI DSS compliance scope.

- Enables secure recurring payments.

- Limits the impact of data breaches.

- Improves transaction security across digital payment channels.

Secure Cryptographic Key Management

Why Is Key Management Important?

Encryption is only as secure as the cryptographic keys used to protect the data. If encryption keys are compromised, even the strongest encryption algorithms become ineffective.

A comprehensive key management strategy ensures that keys are securely generated, stored, distributed, rotated, and retired throughout their lifecycle.

Best Practices for Secure Key Management

- Generate keys using secure cryptographic modules.

- Store keys in Hardware Security Modules (HSMs) whenever possible.

- Implement Remote Key Injection (RKI) for secure key distribution.

- Rotate keys at regular intervals.

- Restrict access using role-based access control (RBAC).

- Monitor key usage through detailed audit logs.

- Immediately revoke compromised or expired keys.

- Establish secure backup and recovery procedures.

Proper key management is essential for maintaining the confidentiality and integrity of payment transactions.

SoftPOS Security Best Practices: Device Attestation, Encryption & MFA

Runtime Application Self-Protection (RASP)

What Is Runtime Application Self-Protection (RASP)?

Even after a SoftPOS application has been securely developed, digitally signed, and deployed, it remains a potential target for cybercriminals. Attackers may attempt to modify the application’s behavior while it is running, extract sensitive information from memory, inject malicious code, or bypass built-in security controls.

Runtime Application Self-Protection (RASP) is an advanced security technology designed to defend the application from within. Unlike traditional security tools that primarily monitor external threats, RASP continuously observes the application’s runtime environment and automatically detects suspicious activities as they occur.

By embedding security directly into the application, RASP enables SoftPOS solutions to identify attacks in real time and respond immediately before sensitive payment information can be compromised.

How RASP Protects SoftPOS Applications

RASP continuously analyzes application behavior during execution and monitors the operating environment for signs of malicious activity. It helps protect against:

Code Injection Attacks

Cybercriminals may attempt to inject unauthorized code into the payment application to manipulate transactions or steal sensitive information.

RASP identifies unauthorized code execution and blocks suspicious processes before they can affect payment operations.

Reverse Engineering

Attackers frequently analyze mobile applications to understand their security mechanisms and identify vulnerabilities. RASP incorporates anti-reverse engineering techniques that make application analysis significantly more difficult. These techniques include:

- Code obfuscation

- String encryption

- Dynamic integrity verification

- Anti-debugging mechanisms

Memory Tampering

Sensitive payment information may temporarily reside in application memory during transaction processing. RASP monitors memory access and detects attempts to:

- Read confidential data

- Modify transaction information

- Inject malicious libraries

- Capture payment credentials

Emulator Detection

Fraudsters often use Android emulators to analyze payment applications. A secure SoftPOS application should detect emulator environments and prevent payment processing on non-genuine devices.

Hooking Framework Detection

Attack tools such as Frida and Xposed attempt to intercept application functions without modifying the application itself. RASP detects these frameworks and blocks payment processing when unauthorized runtime manipulation is identified.

Benefits of Runtime Protection

Implementing RASP provides multiple security advantages:

- Detects attacks while the application is running.

- Prevents unauthorized application modifications.

- Protects sensitive payment information.

- Improves fraud prevention.

- Strengthens compliance with mobile payment security standards.

- Enhances customer confidence in digital payment applications.

Certificate Pinning

What Is Certificate Pinning?

SoftPOS applications frequently communicate with backend services such as payment gateways, Terminal Management Systems (TMS), cloud platforms, and acquiring banks.

Although Transport Layer Security (TLS) encrypts these communications, attackers may still attempt Man-in-the-Middle (MITM) attacks by presenting fraudulent certificates.

Certificate Pinning strengthens communication security by allowing the SoftPOS application to trust only specific, pre-approved server certificates.

If an unexpected certificate is presented, the connection is immediately rejected.

Benefits of Certificate Pinning

Certificate Pinning helps organizations:

- Prevent fake server attacks.

- Reduce Man-in-the-Middle attacks.

- Improve API security.

- Protect merchant credentials.

- Secure payment communications.

- Build stronger trust between devices and backend systems.

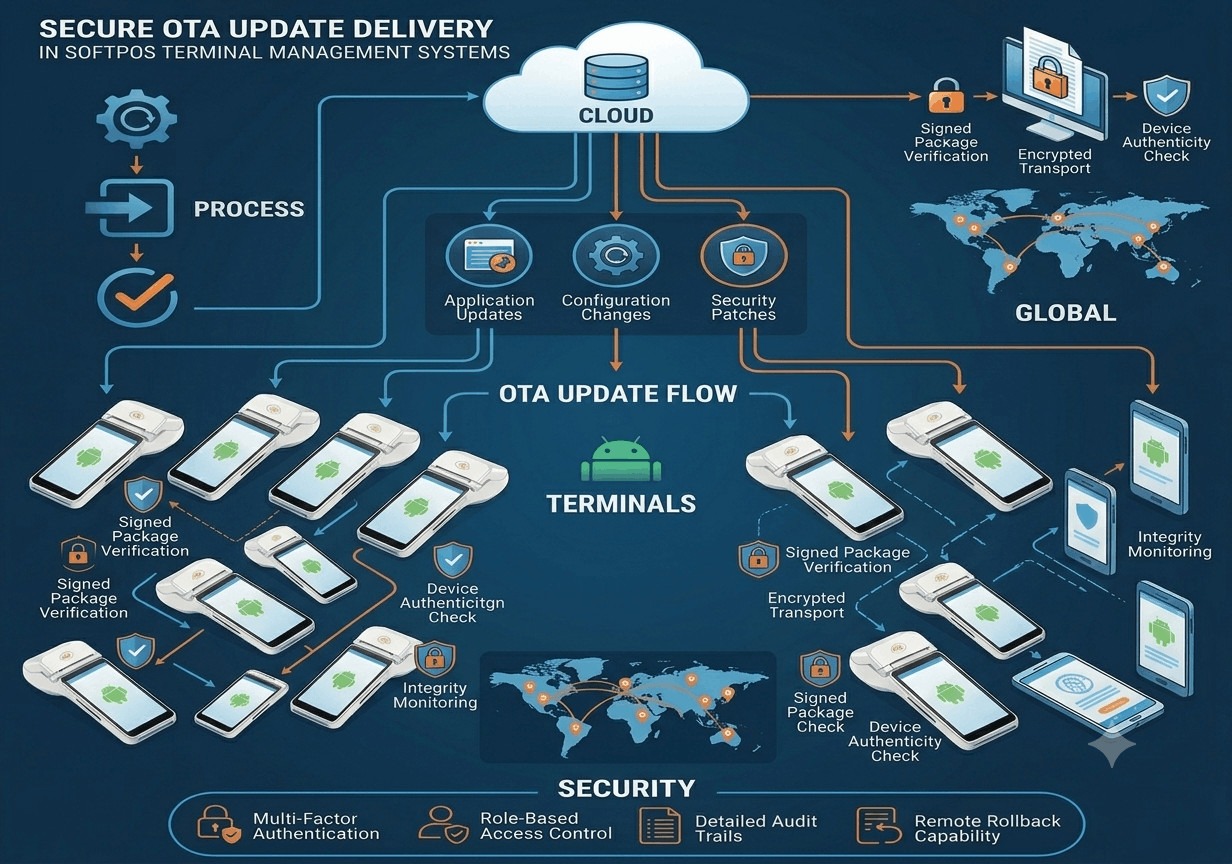

Secure OTA (Over-the-Air) Updates

Why Are OTA Updates Important?

SoftPOS applications require continuous updates to introduce new features, improve performance, patch software vulnerabilities, and maintain compliance with evolving payment standards. However, if software updates themselves are compromised, attackers could distribute malicious applications or altered firmware to thousands of devices. For this reason, OTA updates must be designed with security as a primary consideration.

Security Best Practices for OTA Updates

Organizations should implement several controls to ensure that every update is authentic and trustworthy.

Digitally Signed Updates: Every software package should be digitally signed before distribution. Digital signatures verify:

- Software authenticity

- Publisher identity

- File integrity

Integrity Verification: Before installation, the SoftPOS application should verify that the downloaded package has not been modified during transmission. Integrity checks typically use secure cryptographic hash functions.

Encrypted Distribution: Software packages should be distributed through encrypted communication channels using modern TLS protocols. This prevents attackers from intercepting or modifying update packages.

Version Management: A centralized Terminal Management System should maintain version control across all deployed devices. Benefits include:

- Controlled software rollout

- Automatic rollback

- Update scheduling

- Compliance reporting

Secure Rollback: If an update introduces unexpected issues, administrators should be able to safely restore the previous trusted version without compromising security.

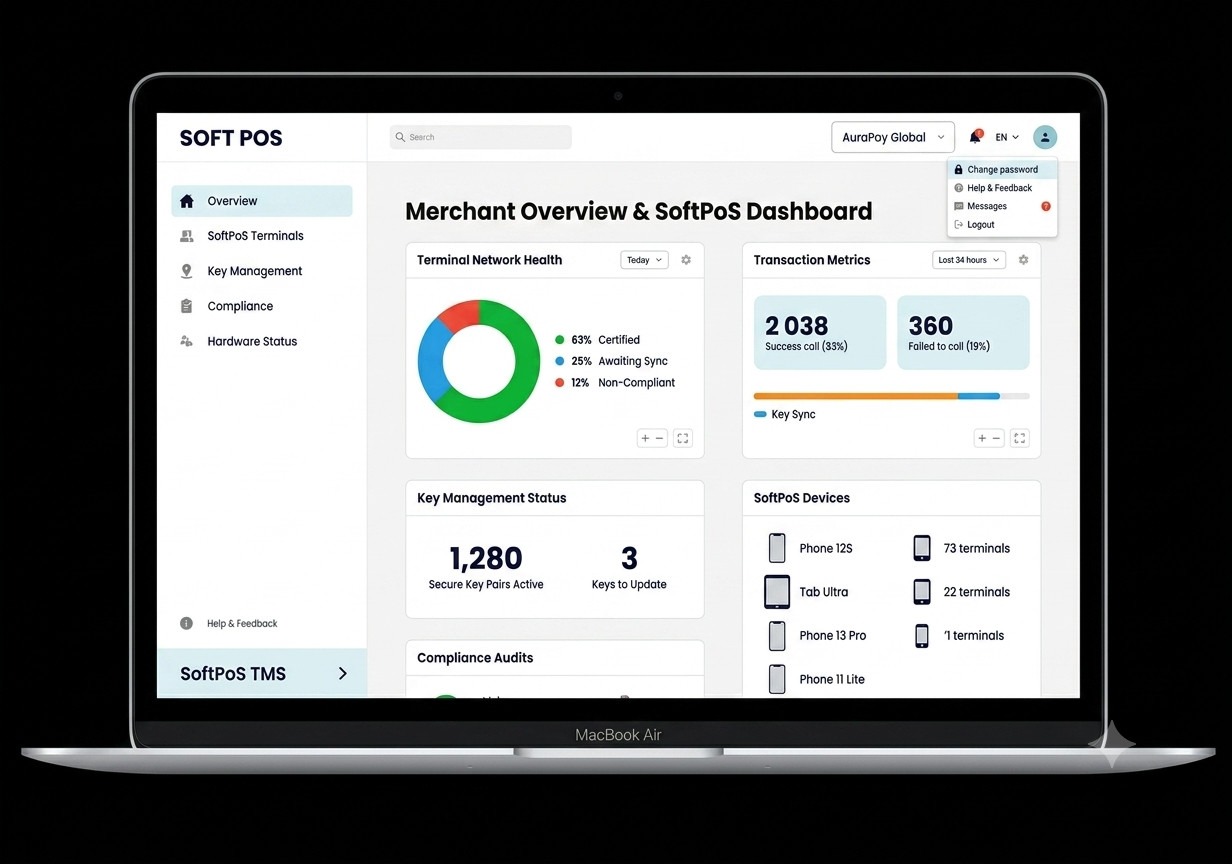

Terminal Management System (TMS) and SoftPOS Security

What Is a Terminal Management System?

A Terminal Management System (TMS) is a centralized platform used to remotely manage, monitor, configure, and secure thousands of SoftPOS devices from a single administrative console.

Instead of manually updating every payment device, administrators can securely control the complete device lifecycle through the TMS.

How TMS Enhances SoftPOS Security

A modern TMS plays an essential role in maintaining payment security throughout the deployment lifecycle.

Remote Device Provisioning

New devices can be securely enrolled and configured without requiring manual installation.

Provisioning includes:

- Merchant activation

- Certificate installation

- Security policy deployment

- Application distribution

Remote Configuration Management

Administrators can remotely update:

- Merchant settings

- Payment parameters

- Network configurations

- Security policies

- Risk management rules

This ensures consistent security across all deployed devices.

Security Policy Enforcement

TMS enables organizations to centrally enforce security requirements.

Examples include:

- Minimum Android version

- Password policies

- MFA requirements

- Certificate expiration

- Device compliance verification

Certificate Management

Managing digital certificates manually becomes increasingly difficult as deployments grow.

TMS automates:

- Certificate issuance

- Certificate renewal

- Certificate replacement

- Certificate revocation

Device Health Monitoring

Continuous monitoring helps administrators identify potential security issues before they become major incidents.

Common monitoring metrics include:

- Battery health

- Network connectivity

- Device location

- Application status

- Security alerts

- Compliance status

Remote Lock and Wipe

If a device is lost or stolen, administrators can remotely:

- Lock the device.

- Remove payment applications.

- Delete sensitive information.

- Disable payment functionality.

These capabilities significantly reduce the risk of unauthorized access.

Role of EMV Kernel in SoftPOS Security

What Is an EMV Kernel?

An EMV Kernel is the software component responsible for implementing the payment logic required to process EMV contact and contactless card transactions. It acts as the bridge between the payment application and the EMV card, ensuring that every transaction follows the rules defined by EMVCo and the supported card schemes.

During a payment transaction, the EMV Kernel performs several critical functions, including application selection, card authentication, risk management, cardholder verification methods (CVM), transaction processing, and secure communication with the payment application. These processes help ensure that payment data is handled consistently and securely across different devices and payment networks.

For SoftPOS deployments, integrating an EMV-compliant Kernel helps maintain interoperability with major card brands while supporting secure contactless payment acceptance. It also provides a strong technical foundation for meeting industry security requirements and delivering a reliable payment experience across diverse merchant environments.

Why EMV Certification Is Important

While implementing an EMV Kernel is essential, organizations must also validate that their payment solution complies with established industry specifications. EMV Certification is the process through which payment devices, software, and applications are tested to verify that they correctly implement EMV standards and interoperate with payment networks.

Certification confirms that payment transactions are processed securely, consistently, and according to the requirements defined by EMVCo and participating card schemes.

Benefits of EMV Certification

Completing EMV Certification offers several operational and security advantages:

- Ensures compliance with global payment standards.

- Improves interoperability across issuers, acquirers, and card brands.

- Reduces implementation and deployment risks.

- Strengthens payment security.

- Supports reliable transaction processing.

- Enhances merchant and customer confidence.

- Facilitates acceptance across domestic and international payment ecosystems.

For banks, fintech companies, payment service providers, OEMs, and system integrators, EMV Certification is a critical step in delivering secure and trusted SoftPOS solutions.

Industry Standards Supporting SoftPOS Security

To maintain a secure and compliant payment environment, organizations should align their SoftPOS deployments with internationally recognized standards and best practices.

Key standards include:

PCI MPoC (Mobile Payments on COTS): Defines security requirements for accepting contactless payments on commercial off-the-shelf mobile devices.

PCI DSS (Payment Card Industry Data Security Standard): Provides comprehensive requirements for protecting cardholder data throughout the payment ecosystem.

EMV Specifications: Establish global standards for secure chip-based payment processing and interoperability across payment networks.

ISO 27001: Defines best practices for implementing and maintaining an effective information security management system (ISMS).

OWASP Mobile Application Security Verification Standard (MASVS)

Provides guidance for developing and assessing secure mobile payment applications.

NIST Cybersecurity Framework: Offers a structured approach for identifying, protecting, detecting, responding to, and recovering from cybersecurity threats.

Following these standards helps organizations strengthen security, reduce compliance risks, and build trusted payment solutions.

Common SoftPOS Security Threats and Their Solutions

Despite implementing multiple security controls, SoftPOS solutions continue to face evolving cybersecurity threats. As payment technologies become more sophisticated, cybercriminals also develop new techniques to exploit vulnerabilities in mobile devices, applications, communication channels, and backend systems.

Understanding these threats allows banks, payment service providers (PSPs), fintech companies, merchants, and software developers to proactively strengthen their security posture.

The following table highlights some of the most common SoftPOS security threats, their potential impact, and the recommended mitigation strategies.

Security Threat | Description | Potential Impact | Recommended Security Controls |

Rooted or Jailbroken Devices | Devices with modified operating systems bypass Android’s built-in security controls. | Data theft, malware infection, unauthorized access. | Device Attestation, Root Detection, Play Integrity API. |

Malware Attacks | Malicious software attempts to steal payment credentials or manipulate transactions. | Card data compromise, fraud, financial losses. | Runtime Protection (RASP), Mobile Threat Detection, Secure App Development. |

Man-in-the-Middle (MITM) Attacks | Attackers intercept communication between the SoftPOS application and backend servers. | Transaction manipulation, credential theft. | TLS 1.3, Certificate Pinning, Mutual Authentication. |

Credential Theft | Weak passwords or phishing attacks expose merchant accounts. | Unauthorized system access. | Multi-Factor Authentication (MFA), Strong Password Policies, Risk-Based Authentication. |

Application Tampering | Hackers modify the payment application to bypass security controls. | Fraudulent transactions, application compromise. | Digital Code Signing, Application Integrity Verification, Anti-Tampering Controls. |

Reverse Engineering | Attackers analyze application code to discover vulnerabilities. | Intellectual property theft, security bypass. | Code Obfuscation, RASP, Anti-Debugging Techniques. |

API Exploitation | Poorly secured APIs become entry points for attackers. | Data breaches, unauthorized transactions. | API Authentication, OAuth 2.0, JWT Tokens, Rate Limiting. |

Encryption Key Compromise | Improperly protected cryptographic keys expose encrypted payment data. | Complete loss of encryption security. | Hardware Security Modules (HSMs), Secure Key Rotation, Remote Key Injection (RKI). |

Stolen Devices | Lost or stolen merchant smartphones may expose payment applications. | Unauthorized payment acceptance. | Device Lock, Remote Wipe, Device Binding, MFA. |

Insider Threats | Unauthorized employee actions may compromise sensitive payment systems. | Data leakage, fraud, compliance violations. | Role-Based Access Control (RBAC), Audit Logs, Least Privilege Access. |

A proactive security strategy combines preventive, detective, and corrective controls to minimize these risks while ensuring business continuity.

SoftPOS Security Best Practices Checklist

Organizations deploying SoftPOS solutions should follow a comprehensive security framework that addresses devices, applications, infrastructure, user authentication, and operational processes.

Device Security

Ensure every payment device is trusted before allowing transaction processing.

Best practices include:

- Perform device attestation before every payment session.

- Block rooted or jailbroken Android devices.

- Verify operating system integrity.

- Enable secure boot where supported.

- Keep Android security patches up to date.

- Register only approved merchant devices.

Application Security

The SoftPOS application should be designed to resist modern attack techniques.

Recommended controls include:

- Digitally sign all application packages.

- Validate application integrity at runtime.

- Implement anti-tampering mechanisms.

- Detect reverse engineering attempts.

- Prevent screen capture where appropriate.

- Secure sensitive application memory.

Data Protection

Payment information should remain protected throughout its lifecycle.

Organizations should:

- Implement End-to-End Encryption (E2EE).

- Encrypt all locally stored payment data.

- Use tokenization instead of storing PAN information.

- Protect cryptographic keys using secure storage.

- Secure all API communications with TLS 1.3.

Identity and Access Management

Unauthorized access remains one of the leading causes of payment fraud.

Security recommendations include:

- Enable Multi-Factor Authentication (MFA) for merchants and administrators.

- Apply strong password policies.

- Use Role-Based Access Control (RBAC).

- Regularly review user permissions.

- Remove inactive accounts promptly.

Network Security

Communication between devices and backend systems must remain confidential and authenticated.

Organizations should:

- Use TLS 1.3 for all communications.

- Implement Certificate Pinning.

- Secure APIs using OAuth 2.0 or JWT authentication.

- Monitor network traffic for suspicious activity.

- Restrict unnecessary network access.

Operational Security

Security should continue after deployment.

Operational best practices include:

- Deploy secure OTA updates.

- Continuously monitor device health.

- Maintain comprehensive audit logs.

- Perform regular penetration testing.

- Conduct vulnerability assessments.

- Train employees on cybersecurity awareness.

Future Trends in SoftPOS Security

As digital payment technologies continue to evolve, SoftPOS security will increasingly rely on intelligent automation, advanced cryptography, and predictive analytics.

Organizations should prepare for several emerging trends that are expected to shape the future of payment security.

Artificial Intelligence (AI)-Powered Fraud Detection

Machine learning algorithms can analyze millions of transactions in real time to identify unusual patterns and detect fraudulent activities before financial losses occur.

AI-based systems continuously improve their accuracy by learning from historical transaction behavior and adapting to new attack techniques.

Behavioral Biometrics

Instead of relying solely on passwords or fingerprints, behavioral biometrics evaluates how users naturally interact with their devices.

Examples include:

- Typing speed

- Touch pressure

- Swipe patterns

- Device movement

- Usage habits

These behavioral indicators provide an additional layer of invisible authentication.

Passwordless Authentication

Future SoftPOS deployments are expected to reduce reliance on traditional passwords by adopting passwordless authentication methods such as:

- Device-based authentication

- Biometric verification

- Passkeys

- FIDO2 standards

Passwordless authentication improves both security and user experience.

Zero Trust Security Architecture

Zero Trust follows the principle of “Never Trust, Always Verify.”

Every device, application, user, and network request must be continuously authenticated and authorized before access is granted.

This approach minimizes the impact of compromised devices and insider threats.

Continuous Compliance Monitoring

Future payment platforms will automatically verify compliance with standards such as PCI MPoC, PCI DSS, and EMV requirements.

Real-time compliance monitoring reduces manual auditing efforts while improving operational efficiency.

Quantum-Resistant Cryptography

Although practical quantum computing is still emerging, payment organizations are already researching cryptographic algorithms capable of resisting future quantum attacks.

Preparing for post-quantum security will become increasingly important over the coming years.

SoftPOS has transformed the payment acceptance landscape by allowing merchants to accept contactless payments using standard NFC-enabled Android smartphones and tablets. While this flexibility offers significant business advantages, it also introduces new cybersecurity challenges that require a comprehensive and proactive security strategy.

A secure SoftPOS deployment is built on multiple layers of protection rather than relying on a single technology. Device Attestation verifies the integrity of payment devices before transactions begin, End-to-End Encryption protects sensitive payment information throughout its lifecycle, and Multi-Factor Authentication strengthens identity verification for merchants and administrators. Additional controls such as Tokenization, Runtime Application Self-Protection (RASP), Certificate Pinning, Secure OTA Updates, Remote Key Injection (RKI), and centralized Terminal Management Systems (TMS) further enhance the overall security posture.

Organizations that adopt these best practices not only reduce the risk of fraud, data breaches, and operational disruptions but also improve regulatory compliance, customer trust, and long-term business resilience. As payment technologies continue to evolve, continuous monitoring, regular security updates, and adherence to global standards such as PCI MPoC, PCI DSS, and EMV will remain essential for maintaining secure and scalable SoftPOS ecosystems.

Building a secure SoftPOS solution requires expertise in payment security, compliance, and EMV technologies. EazyPay Tech offers comprehensive payment technology solutions, including EMV Kernel, EMV Certification, SoftPOS, Terminal Management System (TMS), Remote Key Injection (RKI), Android POS software, and secure payment infrastructure tailored to the needs of banks, payment service providers, fintech companies, OEMs, and system integrators.

Whether you are developing a new SoftPOS platform, upgrading your payment infrastructure, or seeking guidance on EMV compliance and secure transaction processing, our experienced team can help you implement scalable, interoperable, and standards-compliant payment solutions.

Contact EazyPay Tech today to discuss your project and discover how our expertise in EMV technologies and secure digital payment solutions can help accelerate your payment innovation while maintaining the highest levels of security and compliance.