")

The global payments industry has undergone a remarkable transformation in the past three decades, moving away from outdated and vulnerable systems such as magnetic stripe cards and moving toward chip-enabled technologies that provide unparalleled levels of security, interoperability, and efficiency. At the heart of this transformation lies EMV technology, a global standard that fundamentally reshaped the way payment cards are issued, transactions are processed, and fraud prevention mechanisms are enforced across banks, merchants, and financial institutions.

Developed originally in the early 1990s by Europay, MasterCard, and Visa from which the acronym EMV is derived this standard emerged at a time when card fraud had become an increasingly pressing issue, with magnetic stripe cards being especially vulnerable to skimming, counterfeiting, and unauthorized duplication. EMV was designed as a direct response to this problem, introducing a microchip-based solution that not only enhanced security but also laid the foundation for global interoperability and cross-border payment standardization.

While the early adoption of EMV began in Europe, driven by the urgent need to combat fraud, the standard has since spread worldwide, becoming the de facto global framework for secure card-present transactions. The United States, though slower to adopt, embraced EMV in 2015 following the liability shift introduced by card networks, which effectively incentivized merchants and issuers to upgrade their infrastructure. Today, EMV is no longer just about plastic cards; it is a cornerstone of modern payments, powering everything from contactless tap-to-pay transactions and mobile wallets to SoftPOS solutions and biometric authentication systems.

What is EMV?

EMV (Europay, MasterCard, and Visa) is a global standard for smart payment cards and payment terminals that use embedded microchips to authenticate transactions. Unlike traditional magnetic stripe cards, which store static information that can be easily copied, EMV cards generate unique transaction codes, significantly reducing fraud risks.

History and Evolution of EMV

1990s – The Birth of EMV

- EMV was developed in the early 1990s by Europay, MasterCard, and Visa to address the growing issue of card fraud associated with magnetic stripe technology.

- Unlike magnetic stripes, EMV chips introduced dynamic authentication, making it far more difficult for fraudsters to clone cards.

- The first EMV-enabled cards were launched in Europe, where card fraud was rising sharply, prompting early adoption.

2000s – Expansion Across Europe and Asia

- Throughout the 2000s, EMV adoption spread rapidly across Europe, Asia, and Latin America, with many countries making chip-and-PIN the norm.

- Governments, regulators, and banks supported the transition due to the significant reduction in counterfeit and lost/stolen card fraud.

- EMVCo, the body governing EMV standards, was formed to ensure global standardization and continuous updates.

2010–2014 – Global Standardization and Early U.S. Discussions

- By the early 2010s, most major markets outside the U.S. had already migrated to EMV.

- Payment networks began pushing for a worldwide interoperability standard, ensuring EMV cards could be used globally.

- In the U.S., discussions around migration gained momentum, but adoption was slow due to the cost of upgrading POS terminals and ATM infrastructure.

2015 – The U.S. Liability Shift

- A major milestone occurred in October 2015, when Visa, MasterCard, American Express, and Discover enforced the liability shift.

- Under this rule, whichever party (merchant or issuer) had not implemented EMV would be held responsible for fraudulent transactions.

- This policy triggered widespread EMV adoption across retailers, banks, and financial institutions in the U.S.

2016–2020 – Contactless EMV and Mobile Payments

- EMV technology evolved beyond chip-and-PIN to include contactless (tap-to-pay) transactions, offering both speed and security.

- Integration with digital wallets such as Apple Pay, Google Pay, and Samsung Pay further extended EMV’s role in secure mobile payments.

- By this time, over 80% of global card-present transactions were EMV-compliant.

2021–Present – Next-Generation EMV

- EMV is now a universal global standard, powering payments across POS terminals, ATMs, kiosks, SoftPOS (Tap on Phone), and even wearable devices.

- EMVCo continues to release enhancements focusing on contactless performance, biometric authentication, tokenization, and stronger cryptography.

- Today, EMV stands at the center of the digital payment’s ecosystem, reducing fraud while enabling innovation in fintech and mobile commerce.

Key Features of EMV Technology

One of the primary reasons EMV has become a universal standard is the range of advanced features it introduces to protect both consumers and merchants, while enabling convenient and secure transactions. Each feature plays a role in addressing specific weaknesses of earlier payment technologies and strengthening the overall payments ecosystem.

Chip-Based Authentication

At the core of EMV technology is the embedded microchip that replaces the traditional magnetic stripe as the medium for storing and processing payment data. Unlike magnetic stripes, which contain static information that can be easily skimmed and cloned, EMV chips securely store encrypted payment credentials and perform real-time cryptographic processing during each transaction.

This chip-based mechanism ensures that every payment requires communication between the card and the terminal, enabling secure authentication and making counterfeiting attempts ineffective. By leveraging both hardware-based security and algorithm-driven encryption, EMV chips introduced a paradigm shift in protecting cardholder data.

Dynamic Data Authentication (DDA)

One of the most revolutionary aspects of EMV is dynamic authentication, a process that ensures every transaction is unique. Instead of relying on static card numbers or magnetic track data, which could be copied and reused by fraudsters, EMV generates one-time cryptographic codes that cannot be replicated or applied to another transaction.

This process, known as Dynamic Data Authentication (DDA), effectively makes card cloning nearly impossible. Even if a fraudster were able to capture transaction details, they would be useless for future attempts, as the cryptographic code would no longer be valid. This innovation significantly reduced card-present fraud across regions that implemented EMV.

Support for Contact and Contactless Transactions

Another key feature of EMV is its flexibility in supporting both contact transactions (chip-and-dip, where the card is inserted into the terminal) and contactless transactions (tap-to-pay using Near Field Communication, or NFC).

- In contact transactions, the chip establishes a secure, direct connection with the payment terminal, performing authentication and encryption.

- In contactless transactions, the chip communicates wirelessly via NFC, enabling faster payments without sacrificing security.

This dual functionality has been critical in the evolution of modern payments, especially as consumer demand has shifted toward frictionless, touch-free, and mobile-first payment experiences.

Enhanced Cardholder Verification

Security in EMV transactions is not limited to the chip; it also extends to cardholder verification methods (CVMs). EMV supports multiple verification methods, allowing issuers and merchants to balance convenience and security:

- Chip-and-PIN: Requires the cardholder to enter a personal identification number (PIN), providing a strong second layer of authentication.

- Chip-and-Signature: Relies on signature verification, often used in regions where PIN adoption is lower.

- Biometric Verification: As EMV evolves, biometric methods such as fingerprint or facial recognition are being integrated, further enhancing authentication.

This flexibility ensures EMV can adapt to diverse market conditions while maintaining security standards.

Integration with Tokenization

Modern payment ecosystems are not limited to physical cards. With the rise of mobile wallets and digital commerce, EMV seamlessly integrates with tokenization technologies, which replace sensitive card data with randomly generated tokens. These tokens carry no exploitable value if intercepted, further reducing the risk of fraud in both physical and digital environments.

Together, these features have made EMV the gold standard in payment security, global interoperability, and consumer trust.

How EMV Works: A Deep Dive into Transaction Processing

Understanding how EMV functions in practice requires examining the transaction flow for both contact and contactless payments. The process ensures that multiple layers of security are enforced, from the moment the card interacts with the terminal until the bank authorizes the transaction.

Contact EMV Transaction Process

When a customer uses an EMV card by inserting it into a terminal, the following steps occur:

- Card Insertion: The card is inserted into a chip-enabled payment terminal, establishing a secure channel of communication between the chip and the terminal.

- Chip Authentication: The terminal interacts with the card’s embedded chip to confirm its authenticity using cryptographic algorithms. Unlike magnetic stripes, the chip can actively process and respond to security challenges.

- Unique Transaction Code Generation: The chip generates a unique, one-time cryptographic code, ensuring that even if transaction data were intercepted, it could not be reused in another payment attempt.

- Cardholder Verification: Depending on the card and merchant setup, the customer may be required to verify their identity through a PIN, signature, or biometric check.

- Bank Authorization and Completion: The transaction request, along with the unique cryptographic code, is sent to the issuing bank for authentication and approval. Once validated, the transaction is completed, and the card can be safely removed.

This process typically takes longer than swiping a magnetic stripe, but the tradeoff is significantly stronger fraud prevention.

Contactless EMV Transaction Process

For contactless EMV transactions, speed and convenience are prioritized without compromising security:

- Card or Device Tapping: The customer taps the EMV-enabled card or mobile wallet (Apple Pay, Google Pay, Samsung Pay) against an NFC-enabled reader.

- Secure Wireless Data Transmission: The chip wirelessly transmits encrypted transaction data to the terminal within milliseconds.

- Authentication and Approval: Dynamic cryptographic authentication ensures that the payment is legitimate. The transaction is then approved by the issuer in real time.

This method has become particularly popular in retail, public transport, and quick-service environments, where speed is as critical as security.

EMV Transaction Security Mechanisms

The strength of EMV lies in its multi-layered security mechanisms that combine encryption, authentication, and real-time fraud prevention.

Advanced Cryptographic Protection

EMV employs both symmetric and asymmetric encryption to secure sensitive transaction data. By leveraging public key infrastructure (PKI), EMV cards and terminals can authenticate each other, ensuring that the transaction originates from a legitimate source.

Unique Transaction Identifiers

Each transaction generates a unique identifier, often referred to as an application cryptogram. This ensures that even if transaction data is stolen, it cannot be reused, preventing replay attacks and other fraudulent schemes.

Offline and Online Validation

EMV transactions can be validated either:

- Offline, using the chip’s in-built security mechanisms, which is critical in regions with limited internet connectivity.

- Online, requiring issuer bank approval in real time, which provides an additional layer of verification.

This dual approach allows EMV to be effective across diverse environments, from metropolitan cities to remote locations.

Benefits of EMV

The widespread adoption of EMV has delivered tangible benefits to banks, merchants, and consumers alike.

Enhanced Security Against Fraud

By replacing static magnetic stripe data with chip-based encryption and dynamic authentication, EMV has dramatically reduced counterfeit and skimming-related fraud. Regions that adopted EMV early, such as Europe and Canada, saw fraud losses drop significantly.

Reduced Chargebacks and Liability Protection

With the introduction of the liability shift, businesses using EMV-enabled terminals are protected against fraudulent chargebacks. This has reduced financial losses for merchants and encouraged adoption across industries.

Global Standardization of Payment Security

EMV has become a universal standard, enabling seamless cross-border transactions for cardholders and merchants. Whether a customer is traveling in Europe, Asia, or North America, EMV ensures consistent levels of security and interoperability.

Support for Faster, Contactless, and Mobile Payments

The expansion of EMV into contactless and mobile ecosystems has enhanced customer experience, enabled secure tap-to-pay transactions and integrated with digital wallets that offer both convenience and security.

Limitations and Challenges of EMV Adoption

While EMV offers significant advantages, it is not without challenges.

High Implementation Costs

Upgrading infrastructure to support EMV is expensive, particularly for small businesses. Issuers also face costs associated with reissuing millions of chip-enabled cards.

Longer Processing Times

Contact EMV transactions often take longer than traditional magnetic stripe payments due to cryptographic checks. Although contactless technology mitigates this, it remains a concern for high-volume retail environments.

Limited Protection for Card-Not-Present (CNP) Transactions

EMV secures card-present payments, but e-commerce fraud remains a challenge. Online merchants must adopt complementary solutions such as tokenization, CVV checks, and multi-factor authentication.

Slow Adoption in Developing Markets

Some regions struggle to implement EMV due to infrastructure costs and legacy systems, resulting in uneven adoption globally.

Compatibility Issues

Older POS systems may not be compatible with EMV without significant upgrades, and travellers to non-EMV regions may face acceptance issues.

The Future of EMV: Innovations Driving Secure Payments

EMV is not static; it continues to evolve in response to new challenges and opportunities in the payments landscape.

- EMV 3-D Secure (3DS 2.0) : To address online fraud, EMVCo has introduced 3-D Secure 2.0, which incorporates biometric authentication and risk-based analysis to secure e-commerce transactions without adding friction for consumers.

- Biometric Authentication: Future EMV solutions will increasingly integrate biometrics such as fingerprints, facial recognition, and iris scanning, offering stronger and more seamless authentication.

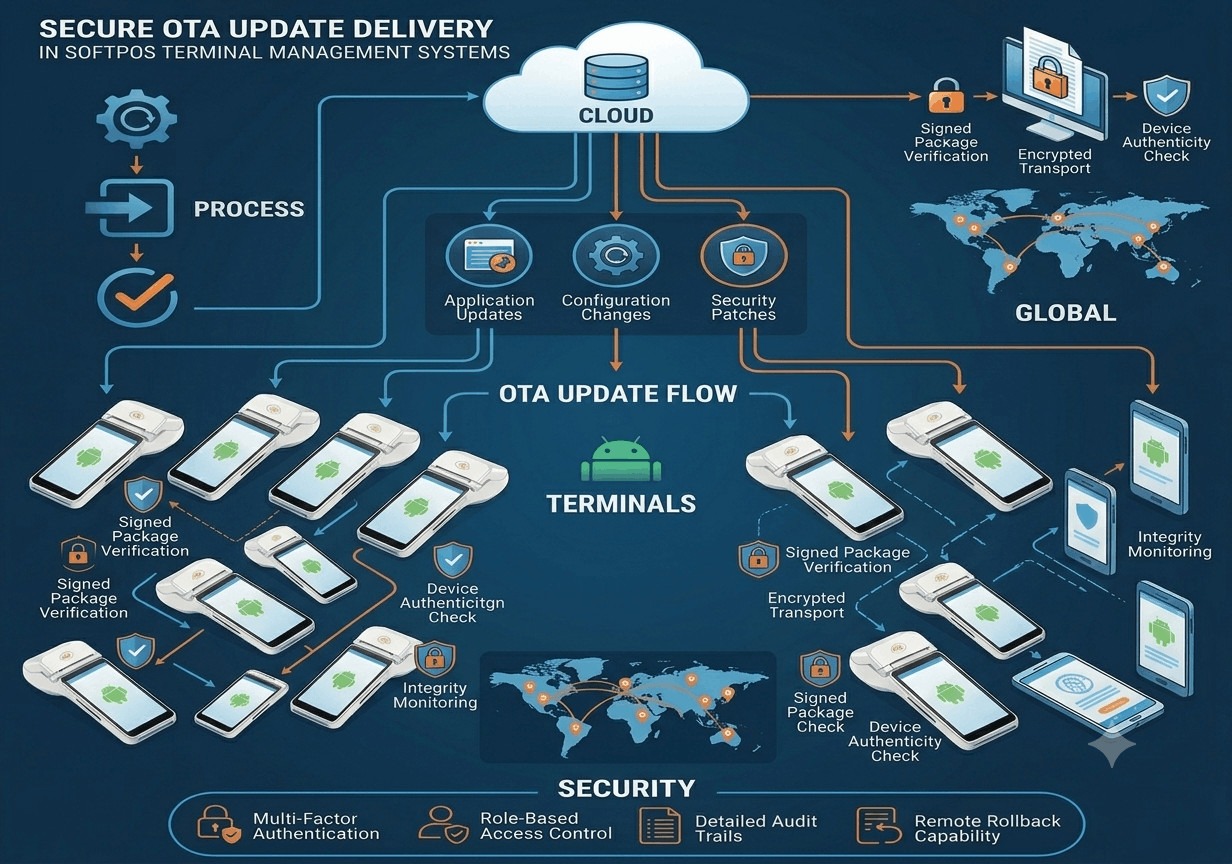

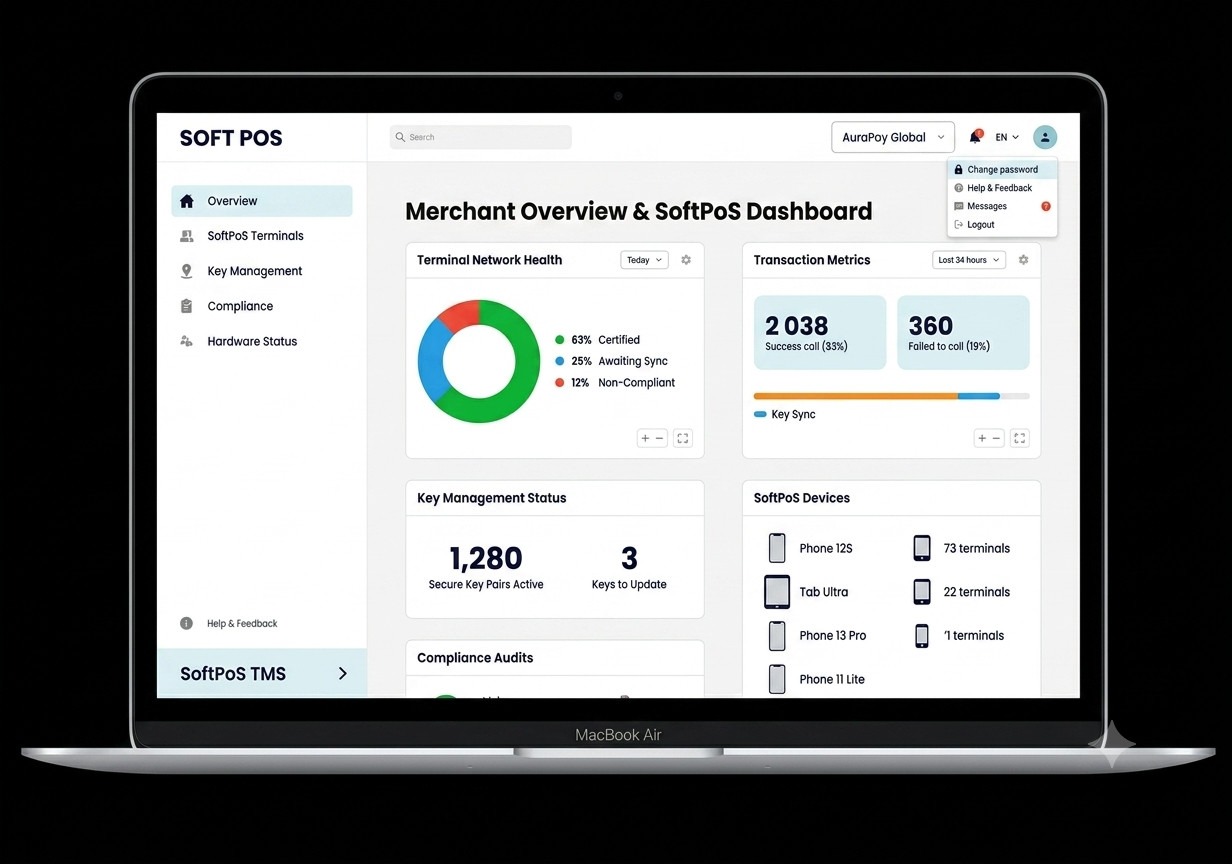

- SoftPOS and Mobile EMV Solutions: The rise of SoftPOS technology allows smartphones to serve as secure payment terminals, enabling small businesses and entrepreneurs to accept EMV transactions without investing in dedicated hardware.

- Expansion of Contactless and Tokenized Payments: With the global shift toward cashless ecosystems, EMV will continue to expand into contactless-first environments, strengthened by tokenization to protect sensitive payment data.

Since its inception in the 1990s, EMV has grown from a regional initiative to a global standard that underpins modern payment security. By introducing chip-based encryption, dynamic authentication, and support for multiple verification methods, EMV has revolutionized the way card-present transactions are secured, reducing fraud and building consumer confidence.

Although challenges such as implementation costs and online fraud vulnerabilities remain, the future of EMV is marked by continuous innovation—from 3-D Secure enhancements and biometric integration to SoftPOS and tokenized ecosystems. For businesses and financial institutions, adopting and upgrading EMV-compliant solutions is not just a regulatory necessity but a strategic imperative to remain secure, competitive, and trusted in the digital economy.

As payment technologies evolve and consumer behaviors shift toward digital-first and contactless preferences, EMV will remain a foundational technology not only preserving transaction integrity but also enabling new forms of secure, convenient, and globally interoperable payments.

For businesses looking to implement EMV technology, EazyPay Tech provides cutting-edge EMV Kernel, EMV certification, EMV Software and payment soundbox solutions tailored to meet the evolving needs of the fintech sector.

FAQ

Europay, Mastercard, and Visa a global standard for smart card payments and secure transactions. It enables chip-based credit and debit cards to communicate with payment terminals, enhancing security against fraud.

EMV has been widely adopted in regions including Europe, Canada, Latin America, Asia, and Africa. The United States has also been transitioning to EMV, with increasing adoption across merchants and financial institutions.

Countries are migrating to EMV to combat counterfeit fraud, enhance payment security, and comply with evolving regulatory requirements. The shift also improves global interoperability of payment cards.

EMV provides several benefits, including:

- Enhanced Security – Reduces fraud by generating unique transaction codes.

- Global Acceptance – Ensures seamless transactions across different regions.

- Supports Contactless & Mobile Payments – Enables faster, more convenient payments.

- Reduces Card Cloning – Makes it difficult for fraudsters to duplicate card data.

EMV chip cards use dynamic authentication, generating a unique cryptographic code for every transaction. Unlike magnetic stripe cards, which use static data, this feature prevents unauthorized duplication and fraud.

The U.S. has been gradually adopting EMV technology since 2015. While most merchants now support chip transactions, some still accept magnetic stripe payments. The migration continues to improve security and reduce fraud.

EMV reduces fraud by:

- Generating one-time transaction codes, preventing reuse of stolen data.

- Supporting PIN authentication, reducing lost or stolen card fraud.

- Limiting counterfeit fraud, as chip data is nearly impossible to clone.

Countries that have implemented EMV have seen significant drops in counterfeit card fraud. For example, after widespread adoption in the UK and Canada, counterfeit fraud decreased by more than 50%.

EMV cards use cryptographic authentication methods such as:

- Offline Data Authentication (ODA) – Verifies card authenticity without connecting to a central server.

- Online Authentication – Uses encrypted communication with the issuing bank.

Cardholder verification methods (CVMs) include:

- Chip and PIN – The cardholder enters a PIN for authentication.

- Chip and Signature – The customer signs to confirm identity.

- Contactless Transactions – Low-value payments may not require additional verification.

Transactions are authorized by the issuing bank using:

- Offline authorization – The card itself determines if the transaction can proceed.

- Online authorization – The terminal connects to the bank for approval.

Contactless EMV payments allow transactions by simply tapping a card on a reader. These payments use the same security features as chip-based transactions, ensuring safety and speed.

Near Field Communication (NFC) technology enables mobile devices to perform EMV transactions. Digital wallets like Apple Pay and Google Pay use EMV security protocols for tap-to-pay transactions.

EMV chip cards help reduce fraud, while PCI DSS (Payment Card Industry Data Security Standard) establishes guidelines for securing payment data. Together, they enhance overall transaction security.

You can visit industry resources such as EMVCo, PCI Security Standards Council, and major card networks like Visa, Mastercard, and American Express for in-depth EMV guidelines and updates.

Banks and financial service providers can work with EMV-certified card manufacturers and payment processors to issue EMV-compliant cards. Partnering with an EMV solution provider simplifies integration and ensures compliance with industry standards.