In the evolving world of digital payments, protecting sensitive cardholder data and preventing transaction fraud are paramount. Two key security frameworks play a central role in safeguarding the payment ecosystem: PCI DSS (Payment Card Industry Data Security Standard) and EMV (Europay, Mastercard, and Visa). While both are essential for reducing the risks associated with electronic transactions, they serve distinct purposes. At EazyPay Tech, we empower businesses by helping them implement both standards with precision—ensuring full compliance, secure operations, and future readiness.

1. What Is PCI Compliance?

PCI Compliance refers to the Payment Card Industry Data Security Standard (PCI DSS), a globally recognized set of security standards established by the PCI Security Standards Council. These standards apply to any organization that stores, processes, or transmits credit card data, regardless of business size. The goal is to protect cardholder information from data breaches, theft, and cyberattacks.

The PCI DSS framework comprises 12 core requirements grouped under six overarching objectives. These include securing networks, encrypting cardholder data, managing vulnerabilities, controlling access to systems and data, monitoring activities, and maintaining an information security policy. Businesses that fail to meet these requirements risk penalties, breach liabilities, and loss of customer trust.

2. What Is EMV Compliance?

EMV Compliance refers to a set of specifications developed by Europay, Mastercard, and Visa that govern how chip-enabled credit and debit cards are processed during in-person transactions. Unlike magnetic stripe cards, EMV cards include a smart chip that generates a unique cryptographic code for every transaction, making it nearly impossible for fraudsters to clone a card.

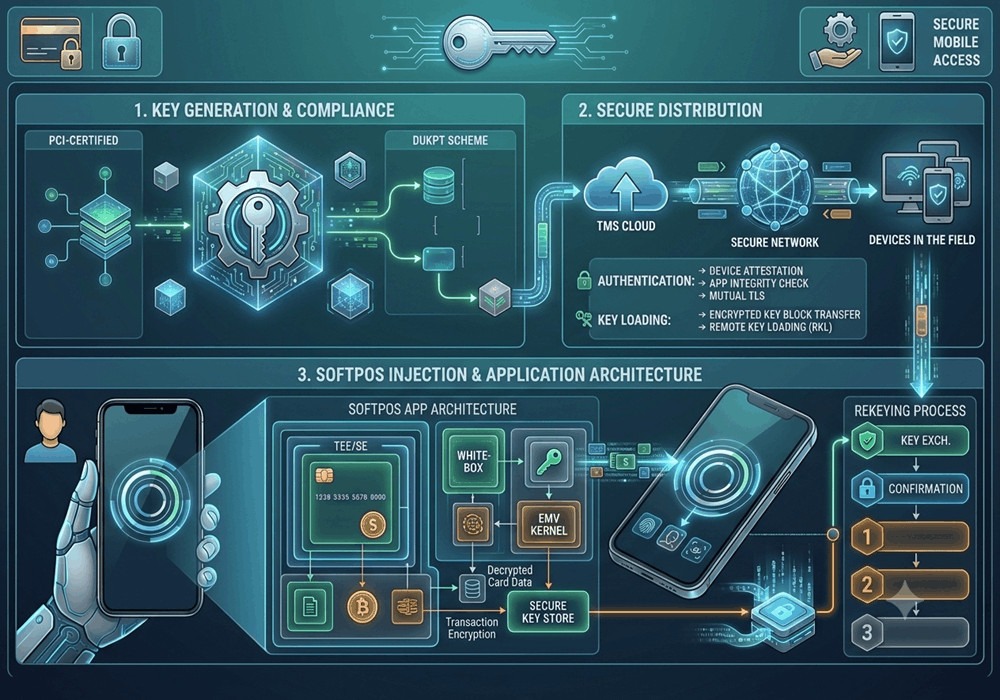

The EMV framework is essential for protecting against counterfeit fraud and ensuring the integrity of card-present transactions. It involves multiple levels of compliance, including EMV Level 1 (hardware compliance), Level 2 (kernel/software compliance), and Level 3 (integration with acquirers and end-to-end testing). While not legally mandatory, EMV adoption is encouraged globally and is often accompanied by a liability shift, meaning merchants may be financially responsible for fraud if they don’t support EMV transactions.

3. The Key Differences Between PCI and EMV

While both PCI DSS and EMV aim to enhance payment security, they differ significantly in scope and application. PCI compliance focuses on data security protecting sensitive cardholder information in storage, during processing and in transit. EMV, on the other hand, is designed to secure card present transactions, preventing in-store fraud through chip-based authentication.

PCI is a mandatory requirement for any business that accepts or stores card data, regardless of the payment channel (e.g., online, mobile or POS). EMV is focused primarily on hardware and software at the point of sale and is crucial for businesses that accept physical card payments.

Understanding the distinction is vital. PCI protects your data; EMV protects your transactions. Together, they form a comprehensive defense against both cyber threats and fraudulent card usage.

4. Why PCI DSS Matters for Your Business

PCI DSS is the cornerstone of data protection in payments. It ensures that all merchants, service providers, and financial institutions maintain systems that reduce the risk of a data breach. PCI applies to a wide range of businesses—from retail stores and e-commerce platforms to software vendors and acquirers.

By following PCI DSS, businesses establish strong encryption protocols, implement firewalls, secure access to payment systems, and maintain logs of network activity. Compliance isn’t just a one-time checklist—it requires ongoing effort, including quarterly scans, annual assessments, staff training, and continuous monitoring.

Non-compliance can result in severe financial penalties, legal action, and loss of the ability to process card payments. At EazyPayTech, we provide businesses with PCI-compliant software, architecture guidance, and security audits to ensure their payment infrastructure meets the highest standards.

5. Why EMV Compliance Matters for Merchants

With the rise of card cloning and counterfeit fraud, EMV chip technology has become the global standard for secure in-person payments. By requiring physical chip presence and dynamic transaction codes, EMV makes it extremely difficult for fraudsters to replicate card data.

EMV compliance helps merchants reduce fraud liability, enhance customer trust, and streamline payment authentication. It also improves interoperability with contactless payments, NFC, and tap-to-pay systems. The liability shift introduced in many countries incentivizes EMV adoption—those who don’t upgrade are financially responsible for any counterfeit fraud at their terminals.

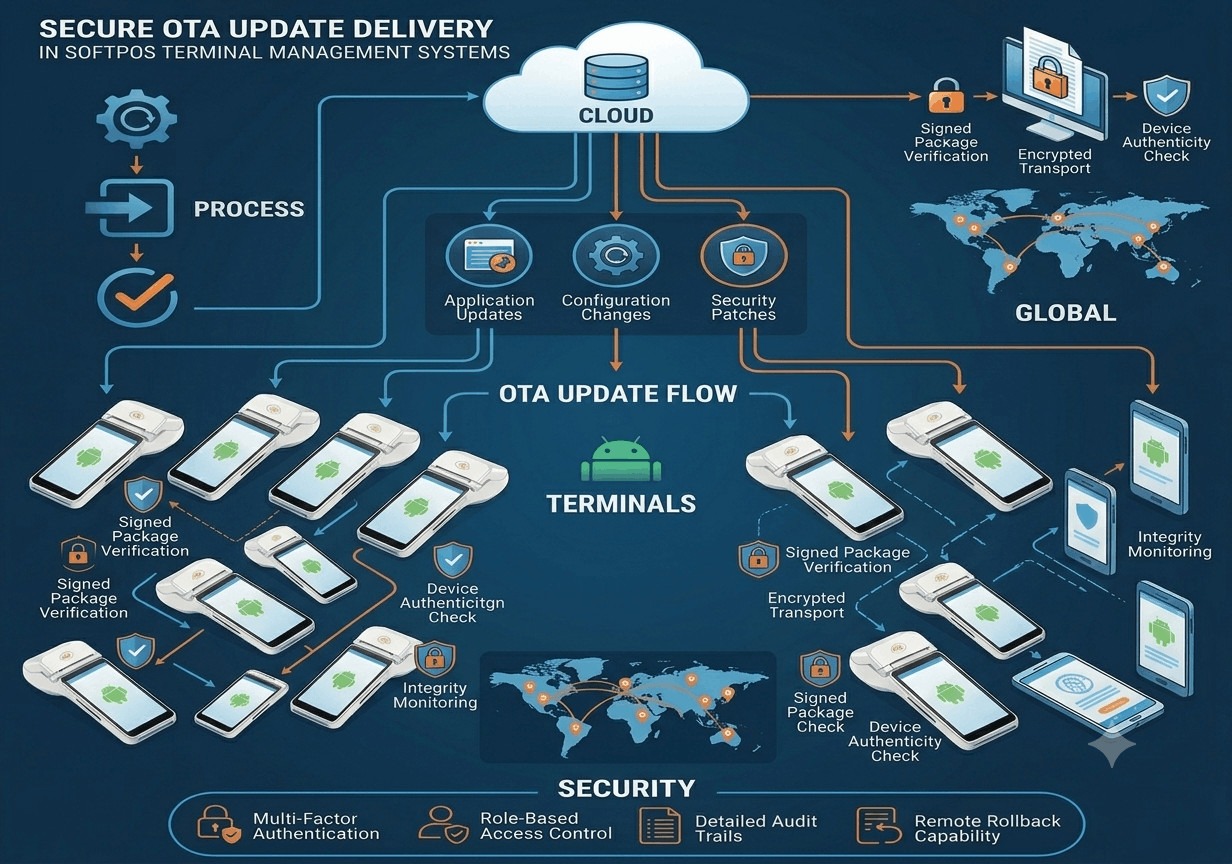

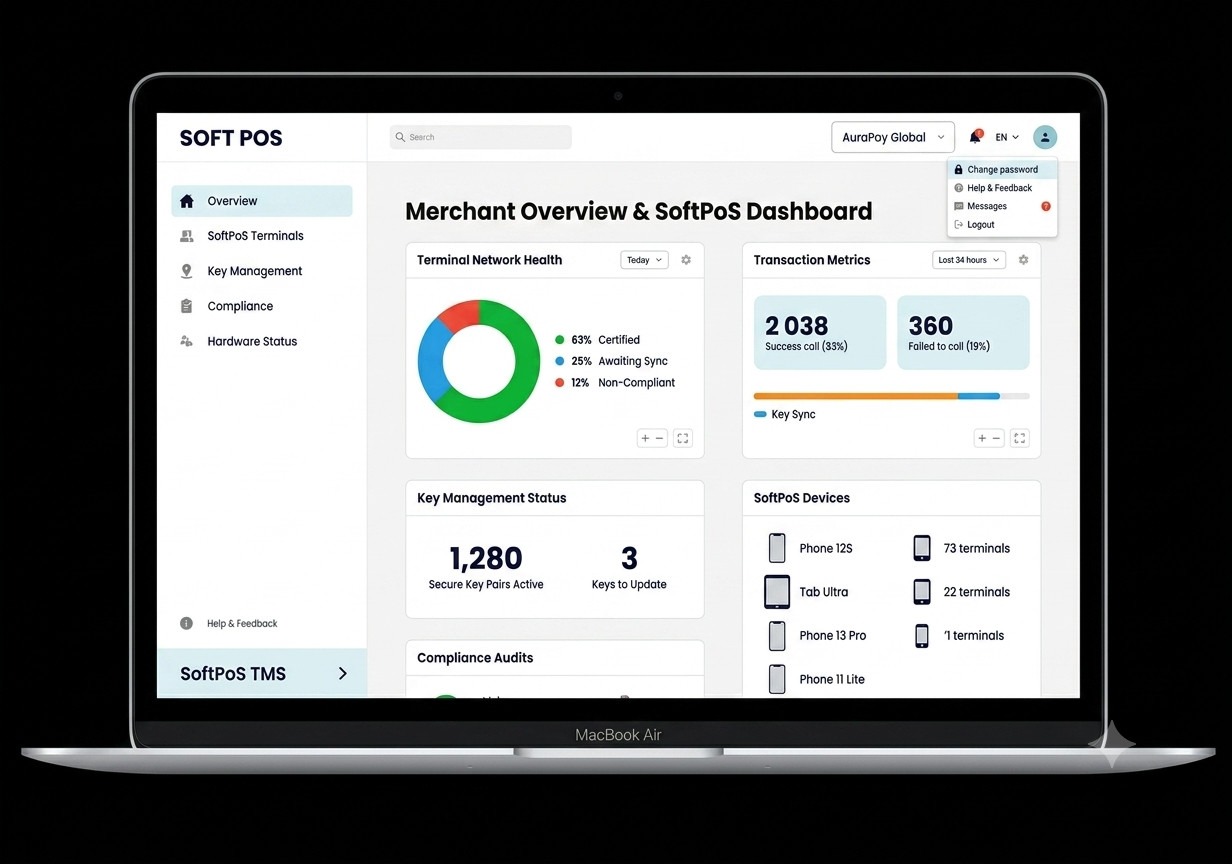

EazyPayTech offers full EMV solutions, including EMV Level 1 and Level 2 kernel development, contactless integration, and support for Level 3 certification—ensuring that your terminals, ATMs, kiosks, and SoftPOS apps meet all technical and regulatory requirements.

6. PCI vs. EMV: Summary of Roles

To simplify:

- PCI DSS is about data security and compliance. It applies across all payment channels and governs how cardholder data is stored, processed, and transmitted.

- EMV is about fraud prevention in face-to-face transactions using chip cards.

- PCI is mandatory for every card-accepting business.

- EMV is not always required, but without it, merchants assume the liability for fraudulent transactions.

At EazyPay Tech, we advise clients never to treat these standards as alternatives—they work best together to create a secure, compliant, and resilient payment environment.

7. Who Needs PCI and EMV Compliance?

The short answer is: almost everyone in the payment ecosystem. If you accept, process, transmit, or store cardholder data, you need PCI compliance. If you operate a physical point of sale, self-service kiosk, ATM, or SoftPOS app, you also need EMV compliance.

This includes:

- Banks and card issuers

- Payment service providers (PSPs) and acquirers

- POS and ATM manufacturers

- Fintech platforms and wallets

- Transport and ticketing systems

- SoftPOS solution developers

- Retailers and large merchants

- E-commerce and hybrid platforms

EazyPay Tech partners with businesses across these segments to ensure smooth implementation of both PCI and EMV frameworks, with pre-certified solutions, consulting, and technical support.

8. How to Become PCI Compliant

Becoming PCI compliant involves several steps depending on your merchant level (determined by your annual transaction volume). The process generally includes:

- Identifying your PCI level

- Completing a Self-Assessment Questionnaire (SAQ)

- Implementing security controls

- Encrypting data transmission and storage

- Running regular vulnerability scans

- Documenting security policies

- Training staff and service providers

As your technical partner, EazyPay Tech provides PCI-ready terminal applications and software platforms that meet all 12 PCI DSS requirements, making it easier to reach and maintain compliance.

9. How to Become EMV Compliant

To achieve EMV compliance, businesses must upgrade their terminals and apps to accept chip card transactions. The process typically includes:

- Installing EMV certified hardware

- Integrating a certified EMV Level 2 kernel

- Completing EMV Level 3 testing with acquirers

- Enabling contactless and tap-to-pay options

- Training staff and customers on usage

EazyPay Tech simplifies this process by offering ready-to-integrate EMV Level 2 kernels for contact and contactless transactions, along with consulting for EMV Level 3 certifications for global markets.

10. Common Misconceptions About PCI and EMV

Several myths cause confusion among merchants and developers:

- Myth 1: EMV makes PCI compliance unnecessary

Truth: EMV only protects against in-person fraud. PCI protects all cardholder data, including in the cloud and mobile apps. - Myth 2: Only large companies need compliance

Truth: All merchants, regardless of size, are subject to PCI DSS. EMV liability applies to everyone accepting card payments. - Myth 3: EMV is too expensive

Truth: EazyPayTech offers cost-effective EMV kernels and SoftPOS SDKs for faster, affordable rollout.

Understanding these facts helps businesses prioritize their security investments effectively.

11. Why Choose EazyPayTech

EazyPayTech is a global leader in providing PCI and EMV security solutions for fintechs, OEMs, issuers, and acquirers. Our offerings include:

- EMV Level 1 and Level 2 Kernels

- PCI DSS-compliant payment terminal applications

- EMV Level 3 testing support

- Contactless and NFC integration

- SoftPOS SDKs and mobile solutions

- Global compliance services for India, Southeast Asia, Africa, Middle East, and Europe

Whether you need help integrating a contact EMV kernel into your POS terminal, enabling PCI compliance for a QR code system, or building a compliant SoftPOS product, EazyPay Tech ensures security, speed, and success.

12. Conclusion: The Power of PCI and EMV Combined

In the fight against fraud, data breaches, and regulatory penalties, businesses cannot afford to rely on only one type of protection. PCI and EMV serve complementary roles—and implementing both is no longer a luxury but a necessity.

- PCI DSS ensures your data systems are secure, monitored, and compliant.

- EMV ensures that your transactions are protected from counterfeit and in-store fraud.

At EazyPay Tech, we help you implement both, guiding your journey toward secure, compliant, and globally accepted payment systems.

Ready to Secure Your Payment Systems?

Let’s talk about how EazyPayTech can help your business with PCI DSS compliance and EMV kernel integration for POS terminals, ATMs, kiosks, and SoftPOS apps.

📧 Email us today

🌐 Visit eazypaytech.com

📞 Schedule a free consultation

Secure every transaction. Certify every solution. Grow with confidence.