In an age defined by speed, safety, and seamless user experiences, contactless payments have emerged as the new norm in global commerce. Once a novelty, they’ve become a necessity. But while tapping a card or phone feels effortless, a sophisticated web of technologies lies beneath each transaction.

Fifteen years ago, making a simple purchase often meant inserting your card into a terminal and entering your PIN, regardless of how small the transaction was. Whether you were buying a coffee or a movie ticket, the authentication process remained the same. That changed dramatically in September 2007, when the first contactless cards were introduced in the UK. With a simple tap, users could now pay in seconds with no PIN, no swipe.

Since then, contactless payments have revolutionized global commerce. In 2020 alone, contactless transactions accounted for nearly a quarter of all point-of-sale payments worldwide. By 2021, that figure had ballooned to a staggering $2.5 trillion in transaction volume. This trend continues upward as contactless becomes not just a convenience, but a global payment standard.

But what powers these seamless taps? What technologies are involved, and how do they ensure safety, security, and speed? Let’s take a deep dive into the core technologies behind contactless payments RFID, NFC, EMV, and QR codes and understand their evolution, use cases, and future applications.

A Brief History of Contactless Payments

The concept of contactless communication began in the 1970s with the invention of smart card technology. By 1979, Michel Hugon had developed a computerized smart card that integrated a processor and local memory. Telecom companies adopted this for SIM cards, while public transport operators leveraged it for contactless travel passes.

In 1995, the first truly contactless cards emerged in South Korea, known as UPass cards, used primarily in public transportation. Fast-forward to 2005, and trials began with contactless payment cards, culminating in Barclaycard’s 2007 release of the UK’s first contactless-enabled debit card, OnePulse.

From there, the contactless ecosystem rapidly evolved:

- 2011: Google Wallet introduced NFC-based mobile payments.

- 2015: Apple enabled smartwatch payments with Apple Pay.

- 2020–2021: The COVID-19 pandemic drove rapid adoption of touch-free payments across the world.

- 2023 and beyond: Tap-to-Phone and SoftPOS (Software Point of Sale) are being widely adopted to convert smartphones into contactless terminals.

Now let’s break down the technologies that make contactless transactions possible.

Core Technologies Behind Contactless Payments

1. RFID (Radio Frequency Identification)

Definition:

RFID is the base technology behind most contactless interactions. It uses radio waves to wirelessly transfer data between a reader and a tag embedded in a card, wristband, or item.

RFID is a technology that uses electromagnetic fields to automatically identify and track tags attached to objects. It consists of three components:

- Tag (transponder) containing a microchip and antenna

- Reader (interrogator)

- Antenna that sends signals between the tag and reader

Frequencies

- Low Frequency (LF): 30 kHz–300 kHz

- High Frequency (HF): 3 MHz–30 MHz (NFC operates here)

- Ultra-High Frequency (UHF): 300 MHz–3 GHz

Working Mechanism

When a tag comes within range of a reader, the tag is energized and transmits its data. RFID tags can be passive (no battery) or active (battery-powered).

Limitations:

RFID lacks encryption and has limited data capacity. It’s excellent for item tracking but not robust enough for secure financial transactions.

Applications

- Inventory management

- Library systems

- Event access control

- Asset tracking

- Anti-theft systems

2. NFC (Near Field Communication)

NFC is a subset of RFID technology but operates at a much higher frequency 13.56 MHz and only works at a range of up to 4 cm. Its short range is actually a security advantage, making it ideal for financial applications.

Purpose-built for short-range, bi-directional communication between two devices. It’s the technology powering most mobile wallets (Apple Pay, Google Pay) and Tap to Pay solutions.

Working Mechanism

NFC supports two-way communication, enabling devices to act as both readers and tags. For example, your smartphone can read contactless cards and also act as a contactless payment device.

Key Features

- Bi-directional communication

- Works without internet

- Fast data exchange

- Built-in encryption standards

Applications

- Contactless mobile payments (Apple Pay, Google Pay, Samsung Pay)

- Ticketing in public transport

- Smart home automation

- Digital business cards

- Access control systems

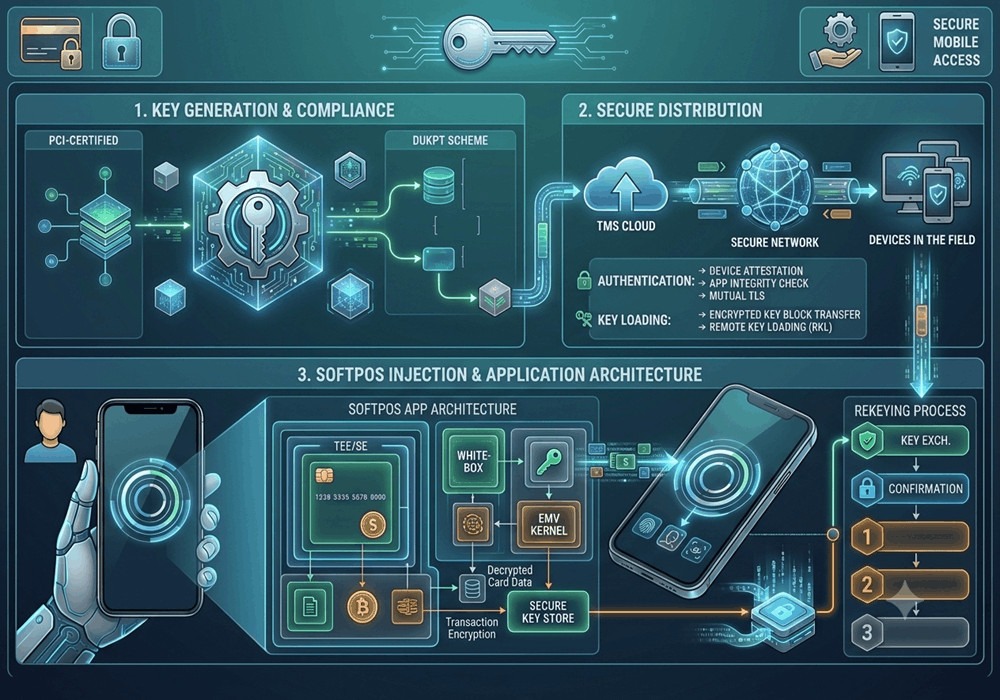

3. EMV & EMV Software

EMV

EMV refers to smart payment cards and terminals that use embedded microprocessor chips for secure payments. EMV ensures that each transaction generates a unique cryptogram, making card cloning significantly more difficult.

EMV Software

EMV software is a critical component in modern payment systems, enabling secure and compliant processing of card transactions across contact, contactless, and mobile platforms. It includes EMV Level 1 and Level 2 kernels that handle communication with chip cards and perform validation, authentication, and risk management as per EMVCo standards.

Designed for use in POS terminals, ATMs, mobile payment devices, and SoftPOS applications, EMV software ensures interoperability with global card schemes like Visa, MasterCard, RuPay, and UnionPay. By leveraging certified EMV software, payment solution providers can accelerate time-to-market, reduce fraud risks, and meet regulatory compliance with confidence.

Types of EMV Transactions

- Contact EMV: Card is inserted into the terminal

- Contactless EMV: Tap-and-go functionality using NFC

- EMV Tokenization: Replaces card data with encrypted tokens

Security Benefits

- Dynamic authentication (unlike magnetic stripe cards)

- Reduced card-present fraud

- PCI DSS compliance

- Secure offline authentication via cryptograms

Applications

- Bank-issued credit and debit cards

- Point-of-sale terminals

- ATMs

- Transit fare cards

- Wearables with embedded EMV chips

4. QR Codes (Quick Response Codes)

QR codes are 2D matrix barcodes that can store over 7,000 numeric characters. First developed in 1994 by Denso Wave (Japan), they have since become instrumental in mobile-based payment ecosystems.

They have emerged as a cost-effective, low-tech contactless payment solution, especially in regions with high mobile penetration but limited POS infrastructure.

How It Works

- The merchant displays a QR code that encodes payment information or links to a checkout portal.

- The user scans the code using a smartphone camera or payment app.

- The transaction is authenticated using digital wallets or bank apps.

Advantages

- No hardware or terminal needed

- Scalable for small businesses and street vendors

- Works on feature phones in certain implementations (e.g., Bharat QR, Alipay)

Applications:

- P2P payments

- Retail and ecommerce checkouts

- Restaurant menus and ordering

- Digital marketing campaigns

- Utility bill payments

Why Contactless Payments Matter

1. Speed and Convenience

Transactions are completed within seconds. No PIN entry or change needed. Customers tap and go—leading to faster checkout lines and higher customer satisfaction.

2. Hygiene and Safety

The pandemic shifted consumer preference to touch-free solutions. Contactless payments reduce the need to handle cash or physical terminals, minimizing germ transmission.

3. Increased Sales Potential

Studies show that faster payment options increase average basket sizes. Customers are more likely to make impulse purchases when checkout is seamless.

4. Enhanced Security

EMV chip cards and tokenized NFC transactions offer superior protection compared to magnetic stripe cards. Each transaction uses a unique cryptogram, making data skimming and cloning much harder.

5. Global Acceptance

From metro systems in Hong Kong to street vendors in Kenya, contactless is becoming the norm. QR code-based payments dominate Asia, while EMV contactless is prevalent in Europe and North America.

EazyPay Tech’s in the Contactless Revolution

At EazyPay Tech, we empower businesses with modern contactless payment solutions that are scalable, secure, and easy to integrate.

Our Key Offerings

A. QR Code Payment Solutions

- Display static or dynamic QR codes at checkout

- Customers can scan using any mobile wallet (Apple Pay, Google Pay, etc.)

- No hardware required—perfect for mobile vendors, freelancers, or small shops

- Real-time transaction confirmations

- PCI-DSS compliant infrastructure

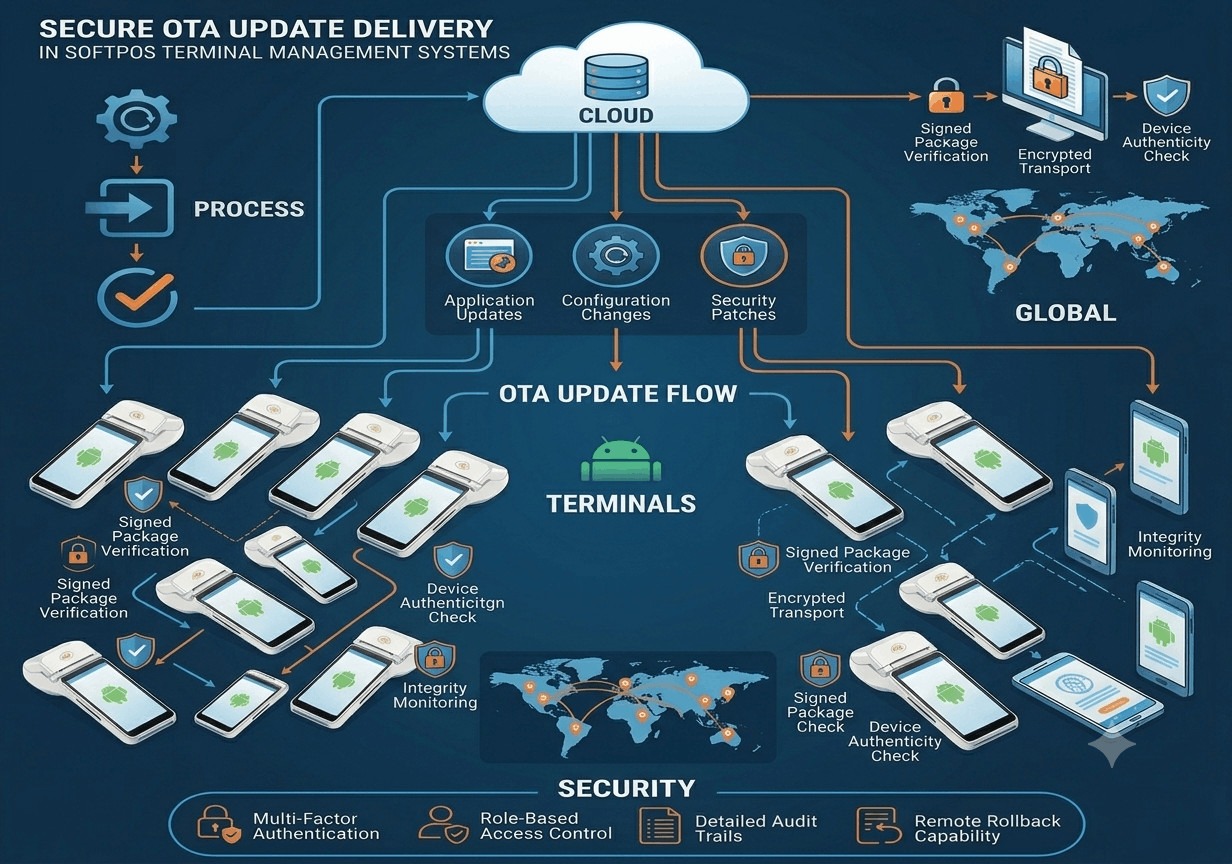

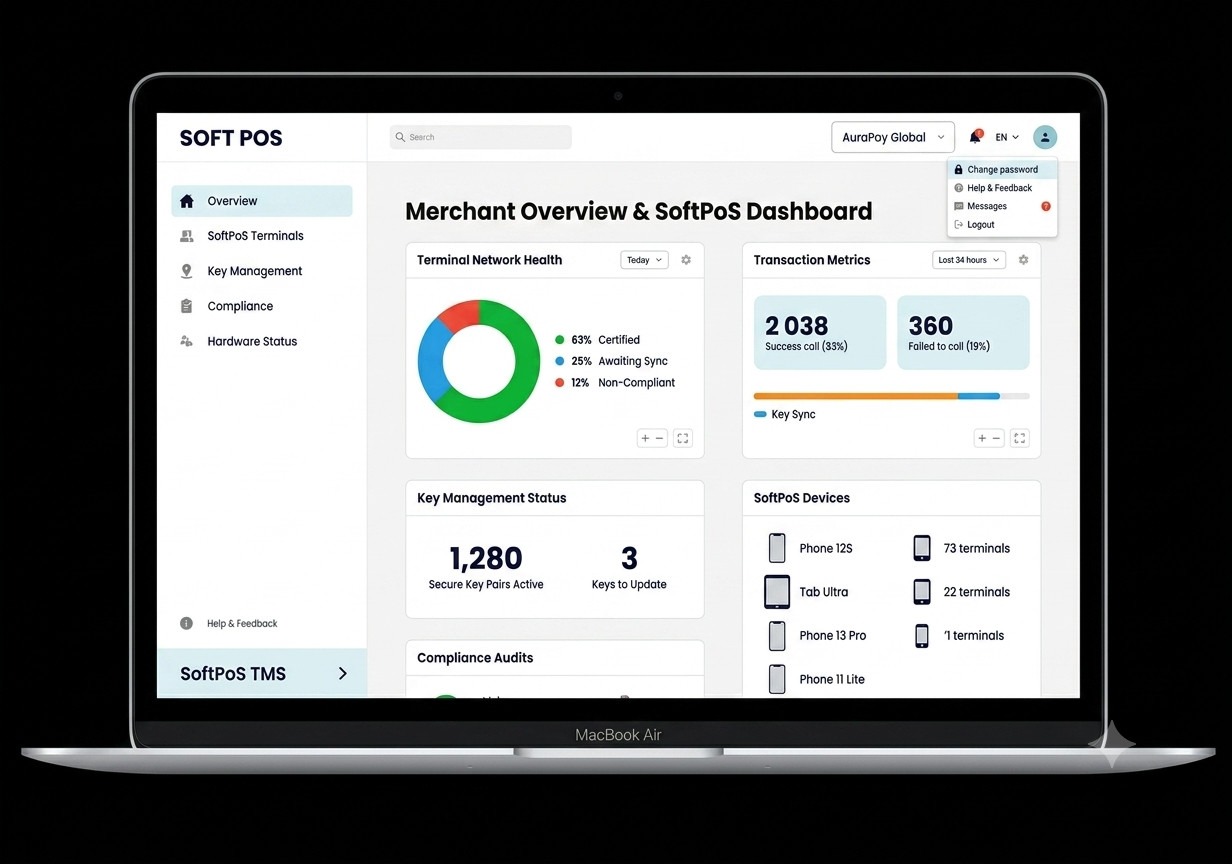

B. Tap to Pay (SoftPOS)

- Transform your Android phone into an NFC-enabled POS terminal

- Accept payments from contactless cards, smartwatches, and phone

- No external device needed—ideal for micro-merchants, delivery agents, and gig workers

- Supports EMV-level encryption and secure transaction processing

- Scheduled for launch in upcoming product cycles

C. EMV Kernel Development and Certification

- EMV L1 & L2 contact/contactless kernel integration

- Testing and certification support for card schemes (Visa, MasterCard, RuPay, etc.)

- Custom SDKs for terminal and mobile integration

- Compliance with PCI, EMVCo, and regional standards

Applications Across Industries

1. Retail

Faster checkouts and reduced queuing time during peak hours improve customer experience and conversion rates.

2. Public Transport

Contactless ticketing systems improve boarding efficiency and reduce cash handling, especially in high-volume metro systems.

3. Hospitality

Hotels and restaurants benefit from quick check-in/out processes and table-side contactless payments.

4. Events and Entertainment

QR-based and NFC wristband payment systems simplify entry and concession stand purchases at concerts or festivals.

5. Financial Services

Banks and fintechs use contactless technology to enhance customer onboarding and payment flexibility across multiple channels.

The Road Ahead: What’s Next for Contactless Payments?

The future of contactless payments is bright and multifaceted:

- Biometric NFC payments: Using fingerprints or facial recognition with contactless

- Wearable devices: Payment rings, bracelets, and embedded chips in clothing

- Cross-border interoperability: Standards that work across multiple card schemes and countries

- Context-aware payments: IoT devices that initiate payments in the background (e.g., smart fridges)

As digital transactions overtake cash globally, businesses need to stay ahead of technological trends to remain competitive.

Whether through RFID tags, EMV chips, NFC smartphones, or QR codes, contactless payment technology has changed the way we live, shop, and move. The blend of speed, convenience, and security makes it not only a preferred method for consumers but a necessary tool for businesses looking to stay competitive in the digital economy.

At EazyPay Tech, we’re not just enabling transactions—we’re building the future of payments. From EMV kernel integration to QR and Tap to Pay solutions, we provide everything you need to go contactless with confidence.

Ready to join the contactless revolution?

Reach out to EazyPay Tech today to discover how we can support your journey toward smarter, faster, and more secure payment systems.